The questions come up constantly in Pakistani communities across the UK. Does money sent from family in Lahore count as income? Does owning a flat in Karachi need to be declared to HMRC? What happens if rental income from a property in Islamabad has been sitting unreported for a few years? Getting the answers wrong or not looking for them at all is where the expensive mistakes happen.

Overseas tax preparation is not just an administrative task for accountants handling complex portfolios. It is a genuine necessity for any UK-based Pakistani who owns property abroad, receives money from family, holds a Pakistani bank account, or has ever inherited land or assets. The rules are specific, HMRC’s visibility into overseas finances has increased significantly, and the consequences of getting it wrong compound quickly.

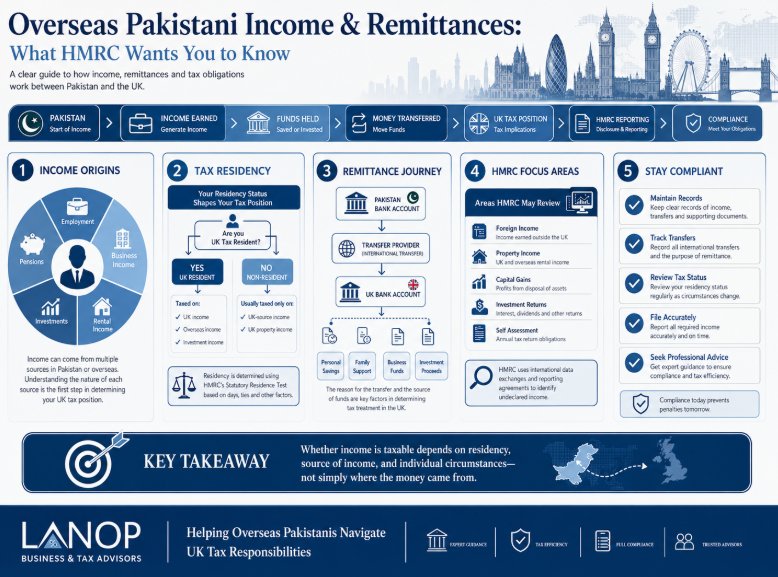

This guide explains how UK tax rules apply to your situation, what actually needs to be reported, and where the most common misunderstandings occur.

Why Your UK Tax Residency Status Is the Starting Point?

Before any conversation about overseas income, one question has to be answered: are you a UK tax resident? The answer drives almost everything else.

HMRC determines tax residency through the Statutory Residence Test, a structured set of rules based on how many days you spend in the UK, where your home is, and where you work. Nationality has nothing to do with it. A Pakistani passport holder who lives and works in Birmingham is almost certainly a UK tax resident. A Pakistani national who splits time between Karachi and London may or may not be, depending on the specifics.

Why does it matter? Because UK tax residents are generally taxed on their worldwide income. That means rental income from a property in Pakistan, interest from a Pakistani savings account, dividends from Pakistani investments all of it potentially falls within HMRC’s scope. Non-residents are taxed differently, primarily on UK-source income only.

The situations that create genuine complexity are the ones in between. Frequent travel between the UK and Pakistan. Working abroad for extended periods. Moving back to Pakistan temporarily. Each of these can affect residency status in ways that are not immediately obvious, and getting the residency question wrong means the entire tax position is built on a flawed foundation.

What Changed in 2025 and Why Older Advice May Be Wrong?

The UK’s taxation of foreign income changed significantly in 2025. The previous remittance basis which allowed certain non-domiciled UK residents to pay tax on overseas income only when they brought it into the UK has been abolished and replaced with a new framework.

Under the current rules, UK tax residents are generally taxed on their foreign income as it arises, regardless of whether that money is ever transferred to the UK. This is a fundamental shift from how things worked before, and a significant volume of online advice including content that still ranks highly in search results reflects the old system rather than the current one.

For overseas Pakistanis who relied on the remittance basis, this change matters enormously. Income that was previously outside HMRC’s reach until it arrived in the UK may now be reportable as it is earned.

What Overseas Income Must Be Reported?

The categories of foreign income that UK tax residents typically need to declare include:

Rental income from property in Pakistan. If you own property in Pakistan that generates rent, that income is reportable to HMRC. Tax paid in Pakistan on the same income may qualify for relief under the double taxation agreement between the UK and Pakistan but the reporting obligation exists regardless.

Interest from Pakistani bank accounts. Many overseas Pakistanis maintain savings accounts in Pakistan. Interest earned on those accounts is foreign income that falls within the UK tax net for residents.

Dividends from overseas investments. Shares held in Pakistani companies, unit trusts, or other investment vehicles generate dividend income that is generally reportable.

Foreign employment income. Income earned from working in Pakistan, even temporarily, may need to be declared depending on residency status and the nature of the work.

Overseas pension income. Pension payments received from Pakistani government or private schemes are foreign income and need to be considered in the context of the UK return.

The Income People Most Commonly Forget

Beyond the obvious categories, several sources of overseas income are regularly overlooked not through deliberate concealment but through genuine unawareness.

Jointly owned family property is one of the most common. A property inherited by several siblings in Pakistan, generating rental income that is collected by one family member and distributed informally, may still create a reporting obligation for UK-resident siblings on their share. The fact that the money never arrives in the UK bank account does not eliminate the obligation under current rules.

Shared investment accounts, overseas savings held in a spouse’s name, income from a family business, and foreign pension arrangements all fall into this category. The rule of thumb is straightforward: if you are a UK tax resident and you have an entitlement to income generated outside the UK, it is worth establishing whether it needs to be declared before assuming it does not.

Are Remittances from Pakistan Taxable?

This is the question that causes more confusion than almost any other. The honest answer is: it depends entirely on what the money represents.

| Scenario | Is It Taxable? | Key Consideration |

| Transferring personal savings you already owned | Generally no | Must be demonstrably pre-existing capital |

| Receiving money from parents as a gift | Generally no | Gifts are not income but large amounts may prompt questions |

| Bringing inheritance money to the UK | Generally no | Probate records and documentation are important |

| Transferring proceeds from selling land in Pakistan | Possibly | Capital gain may be reportable depending on residency and timing |

| Moving rental income earned in Pakistan | Yes | Foreign income reportable as it arises under current rules |

| Receiving payment for work done in Pakistan | Yes | Employment or self-employment income regardless of where paid |

The critical distinction is between capital and income. Moving your own money savings you accumulated before becoming a UK resident, for example, is generally not a taxable event. Bringing in income that was earned while you were a UK resident is a different matter entirely.

A transfer of £50,000 from a Pakistani bank account to a UK account is not automatically taxable. But HMRC may want to understand what that money represents, particularly if it is a large or regular transfer.

Can HMRC See Your Pakistani Bank Account?

More than most people assume. Pakistan participates in the Common Reporting Standard (CRS), the international framework under which financial institutions in over 100 countries share account information with tax authorities. Pakistani banks report details of accounts held by non-residents to the relevant tax authority, which then shares that information with HMRC where applicable.

This does not mean HMRC has real-time access to Pakistani bank statements. What it means is that account balances and interest information can be exchanged, and HMRC can request further information where discrepancies arise between declared income and financial activity.

The practical implication is straightforward. The assumption that overseas bank accounts are invisible to HMRC is no longer reliable, and has not been for several years.

UK Tax Rules for Pakistani Rental Property

Owning rental property in Pakistan as a UK tax resident creates a clear reporting obligation. The rental income is foreign income, taxable in the UK under Self Assessment. Tax already paid in Pakistan on the same income can typically be credited against the UK liability under the double taxation agreement, which prevents being taxed twice on the same amount.

The mistakes that arise in this area follow a consistent pattern. Rental income is not declared because the owner assumes tax paid in Pakistan covers everything. Or income is declared but Pakistani tax paid is not claimed as relief, resulting in an unnecessarily high UK bill. Or the property is sold and the capital gain goes unreported because the owner did not realise gains on overseas property needed to be declared.

Records matter significantly here. Rental agreements, receipts for expenses related to the property, evidence of tax paid in Pakistan, and documentation of the original purchase price are all important when the UK return is prepared.

What UK Residents Need to Know?(Selling Property in Pakistan)

When a UK tax resident sells property in Pakistan, the gain broadly the sale price minus the acquisition cost may be subject to UK Capital Gains Tax. The fact that the property was in Pakistan, that Pakistani CGT was also paid, or that the proceeds never came to the UK does not remove the potential UK reporting obligation.

Double taxation relief is available here too, but the mechanics require care. The gain needs to be calculated in sterling using exchange rates at the relevant dates. Any Pakistani tax paid on the same gain is credited against the UK liability. Documentation of the original purchase, costs of improvement, and the sale transaction are all needed to calculate the gain correctly.

The most common mistake is assuming the sale does not need to be declared at all. The second most common is declaring it without claiming the relief for Pakistani tax paid.

Double Taxation Relief: Avoiding Being Taxed Twice

The UK and Pakistan have a double taxation agreement that prevents the same income being fully taxed in both countries. The mechanism is a credit tax paid in Pakistan on qualifying income reduces the UK tax liability on that same income.

| Income Type | Taxable in Pakistan? | Reportable in the UK? | Relief Available? |

| Pakistani rental income | Yes | Yes | Yes,credit for Pakistani tax paid |

| Pakistani bank interest | Yes | Yes | Yes,subject to agreement terms |

| Capital gain on property sale | Yes | Yes | Yes,credit applies |

| Gift received from family | No | No | Not applicable |

| Inheritance received | No | No | Not applicable |

| Employment income (Pakistani source) | Yes | Yes | Yes depending on circumstances |

The relief does not always eliminate UK tax entirely. Where Pakistani tax rates are lower than UK rates, there may be a residual UK liability. Where they are higher, the credit is capped at the UK tax due on that income HMRC does not refund the excess.

The Most Common Mistakes Overseas Pakistanis Make

Assuming all remittances are tax-free regardless of their source. Ignoring interest on Pakistani bank accounts because the amounts feel small. Forgetting rental income on property managed by a relative in Pakistan. Believing HMRC cannot access overseas financial information. Missing Self Assessment deadlines because the obligation to file was not recognised in the first place.

Misunderstanding residency status sits underneath most of these. A person who believes they are not a UK tax resident when they are will make all of the above mistakes simultaneously.

Poor record-keeping is the final layer. Without documentation of overseas income, tax paid abroad, property transactions, and the nature of transfers, preparing an accurate return or defending one under HMRC inquiry becomes significantly more difficult.

Practical Checklist Before Filing Your UK Tax Return

“Getting this right consistently is what structured overseas tax preparation actually delivers not just filing a return, but knowing which income sources to include, which relief to claim, and which records to keep before HMRC ever asks.”

- Confirm your UK tax residency status for the relevant tax year

- List every source of overseas income including property, bank accounts, investments, and pensions

- Gather evidence of tax paid in Pakistan on each income source

- Check whether any property was sold and calculate the gain

- Review bank account interest earned during the year

- Confirm the nature of any large transfers received from Pakistan

- Organise receipts, rental agreements, and supporting documents

- Check whether previous years may need to be reviewed

Frequently Asked Questions

I own a property in Pakistan. Do I need to declare the rental income even if I never brought the money to the UK?

Yes. Under current 2025 rules, the previous remittance basis no longer applies for most people. If you are a UK tax resident, rental income from Pakistani property is reportable to HMRC as it arises regardless of whether the money ever reaches a UK bank account. Pakistani tax already paid on that income can be credited against the UK liability, but the reporting obligation exists independently.

My parents in Pakistan regularly send me money to help with living costs. Is that taxable?

Genuine gifts from family members are not treated as income and are not subject to UK Income Tax. However, the nature of the payment matters. If HMRC questions a large or regular transfer, being able to demonstrate it was a gift rather than payment for services or undeclared income is important. Keep records of the transfers and any written confirmation from your parents.

I sold inherited land in Pakistan last year. Do I need to tell HMRC?

Possibly yes. If you were a UK tax resident at the time of sale, the capital gain may be subject to UK Capital Gains Tax reporting. Pakistani tax paid on the same gain can be credited against the UK liability. The key records you need are the probate valuation at the time of inheritance and the sale documentation, both converted to sterling at the relevant exchange rates.

I have a savings account in Pakistan. Does HMRC know about it?

More than most people assume. Pakistan participates in the Common Reporting Standard, through which Pakistani banks can share account and interest information with HMRC. Assuming overseas accounts are invisible to HMRC is no longer a safe position. Interest earned on Pakistani savings accounts is foreign income that UK tax residents are generally required to declare.

I think I have unreported overseas income from previous years. What should I do?

Act sooner rather than later. HMRC’s voluntary disclosure process results in significantly lower penalties than waiting for the authority to identify the issue independently. Review previous years, identify what should have been declared, calculate any tax and interest owed, and make a disclosure through the appropriate HMRC channel. The longer unreported income sits, the more interest accumulates and the higher the penalty range becomes.

Conclusion

Cross-border tax obligations between the UK and Pakistan are more visible to HMRC than most people assume. Residency status determines what needs reporting. Foreign income, remittances, and overseas property all carry obligations that need to be understood and managed correctly.

Lanop Business and Tax Advisors helps overseas Pakistanis across the UK review residency positions, identify reportable income, claim double taxation relief, and file accurate returns. If your overseas financial position has never been properly reviewed, Lanop is ready to help.